Last updated: May 1, 2026

Estimated reading time: 28 minutes

Key takeaways:

- FICO Scores are widely used by lenders, especially in traditional lending decisions.

- VantageScore is also used in the marketplace and is commonly shown by free credit monitoring tools.

- Your FICO Score and VantageScore may be different, even if they are based on information from the same credit bureau.

- A lender may use a different scoring model than the one you see through a free app.

- Newer scoring models, including FICO 10T and VantageScore 4.0, are increasingly important because they can consider credit behavior patterns over time.

- The best way to support both types of scores is to focus on accurate credit reporting, on-time payments, lower credit card balances, responsible account management, and regular credit report reviews.

When people talk about credit scores, they often assume everyone has one single number that all lenders see. In reality, consumers can have multiple credit scores depending on the scoring model, credit bureau, and date the score is calculated. You may check your score through a free credit monitoring app and see one number, then apply for a mortgage, car loan, credit card, or apartment and discover that the lender is using a different score.

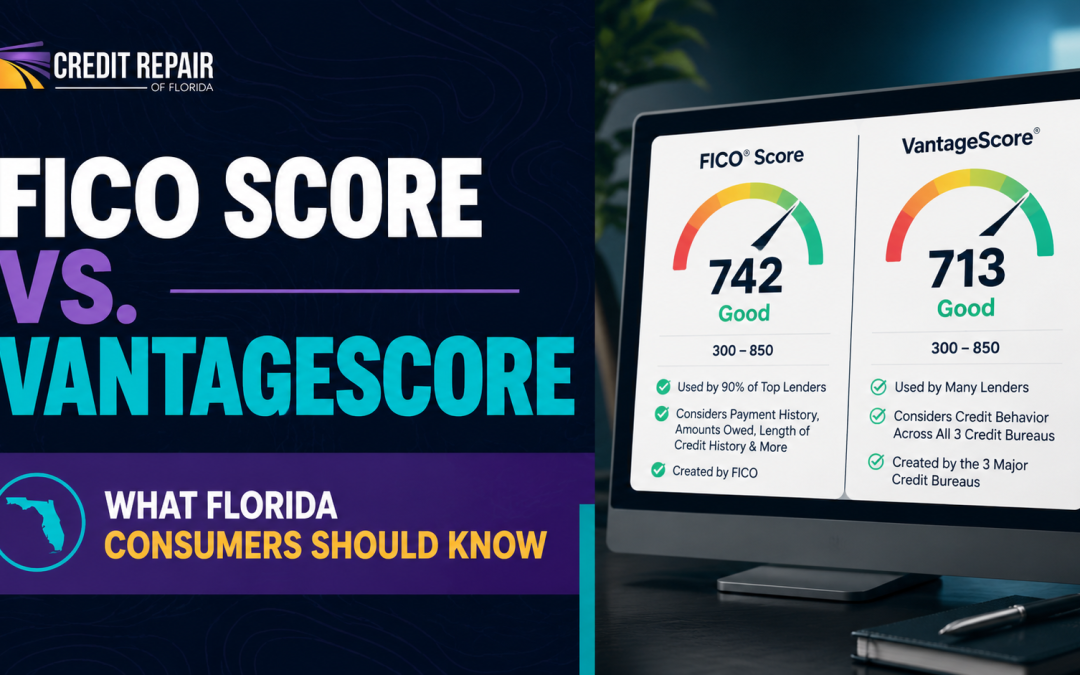

Two of the most common credit scoring models are FICO Score and VantageScore. Both are designed to help lenders evaluate credit risk, but they are not the same. They may use similar score ranges, but they can weigh credit report information differently.

Understanding the difference matters because lenders, credit card companies, mortgage companies, auto finance companies, landlords, insurers, and financial platforms may rely on different scoring models. A score you see online can be useful for monitoring your credit health, but it may not be the exact score used in a lending decision.

For Florida consumers, this is especially important when preparing to buy a home, finance a vehicle, refinance debt, rent an apartment, or review credit report errors. Your credit score may affect approval decisions, interest rates, loan terms, deposits, and other financial opportunities.

This guide explains the key differences between FICO Score and VantageScore, why your scores may not match, which scores lenders may use, and how to build stronger credit over time.

What Is a Credit Score?

A credit score is a three-digit number calculated from information in your credit reports. It is designed to help lenders estimate how likely you may be to repay borrowed money as agreed.

- Credit scores are not random numbers. They are based on credit report data, such as:

- Your payment history

- Your credit card balances

- Your credit limits

- Your account ages

- Your mix of credit accounts

- Recent credit applications

- Collections, charge-offs, or other negative items

- Public record information that may appear on your credit file

Because credit scores are based on credit report information, the accuracy of your credit reports matters. If your reports contain inaccurate, outdated, incomplete, duplicated, or unverifiable information, your scores may be affected.

In the United States, the three major credit bureaus are Equifax, Experian, and TransUnion. These companies collect and maintain credit information reported by lenders, creditors, debt collectors, and other data furnishers. FICO and VantageScore use information from credit reports to calculate scores, but they do so using different scoring formulas.

This is one reason you may have more than one credit score. You do not have just one score. You may have many credit scores depending on the scoring model, the credit bureau data used, the scoring version, and the date the score was calculated.

What Is a FICO Score?

A FICO Score is a credit score created by the Fair Isaac Corporation, commonly known as FICO. FICO is one of the most recognized names in credit scoring and has been used in lending for decades.

Many lenders use FICO Scores when evaluating applications for credit cards, auto loans, personal loans, mortgages, and other financial products. However, there is not only one FICO Score. There are different FICO scoring versions, and lenders may use different versions depending on the type of credit being requested.

For example, a credit card issuer may use one FICO model, while a mortgage lender may use a different FICO model. An auto lender may use an industry-specific FICO Auto Score. This means the score you see from one source may not be the exact same score a lender sees.

FICO Scores commonly range from 300 to 850. A higher score generally suggests lower credit risk, while a lower score may suggest higher credit risk. However, each lender sets its own approval standards. A score that qualifies you with one lender may not qualify you with another.

FICO scoring models generally consider five broad categories:

- Payment history

- Amounts owed

- Length of credit history

- Credit mix

- New credit

Payment history and amounts owed are especially influential. This is why late payments, high credit card balances, collections, charge-offs, and other negative information can have a meaningful impact on your score.

What Is VantageScore?

VantageScore is another credit scoring model. It was created through a joint effort by the three major credit bureaus: Equifax, Experian, and TransUnion.

Like FICO, VantageScore is designed to help lenders evaluate credit risk. VantageScore models also commonly use a 300 to 850 range. However, VantageScore does not use the exact same formula as FICO.

Many consumers first encounter VantageScore through free credit monitoring apps, banking dashboards, credit card portals, and financial education tools. That can be helpful because it gives consumers a way to monitor general credit health. However, it can also create confusion when the score shown in an app does not match the score used by a lender.

VantageScore has released multiple versions, including VantageScore 3.0 and VantageScore 4.0. VantageScore 4.0 is especially important because it uses trended credit data, which can look at patterns in a consumer’s credit behavior over time.

For example, trended data may help show whether a consumer is paying balances down, keeping balances stable, or steadily increasing debt. This can provide a different view than a single snapshot of credit information on one date.

FICO Score vs. VantageScore: Quick Comparison

Here is a simple comparison:

| Category | FICO Score | VantageScore |

|---|---|---|

| Common score range | 300 to 850 | 300 to 850 |

| Created by | Fair Isaac Corporation | Developed by Equifax, Experian, and TransUnion |

| Common use | Widely used by lenders | Used by lenders and many credit monitoring platforms |

| Scoring versions | Multiple versions, including FICO 8, FICO 9, FICO 10, FICO 10T, and industry-specific models | Multiple versions, including VantageScore 3.0 and VantageScore 4.0 |

| Credit history requirements | May require more established credit history, depending on the model | May score some consumers with thinner credit files |

| Data used | Credit report data | Credit report data |

| Model differences | Weighs credit factors using FICO formulas | Weighs credit factors using VantageScore formulas |

| Mortgage relevance | FICO has historically played a major role in mortgage lending | VantageScore 4.0 is becoming more relevant in mortgage credit score modernization |

Both scoring models are important. However, they are not interchangeable. A 700 FICO Score and a 700 VantageScore may not mean the exact same thing to every lender because they are calculated differently.

Why Your FICO Score and VantageScore May Be Different

It is common for consumers to see different credit scores from different sources. This does not automatically mean something is wrong. Several factors can explain the difference.

1. The scoring formulas are different

FICO and VantageScore use different mathematical models. They may consider many of the same types of credit report information, but they may weigh that information differently.

For example, both models care about payment history and credit utilization, but the exact impact of a late payment or high balance may not be identical.

2. The score may be based on different credit bureau data

Your Equifax, Experian, and TransUnion credit reports may not be identical. One lender may report to all three bureaus, while another may report to only one or two. A collection account may appear on one report but not another. A balance update may show on one bureau before it appears on the others.

Because of these differences, a score based on Experian data may differ from a score based on TransUnion or Equifax data.

3. The scoring version may be different

There are many versions of FICO and VantageScore. For example, FICO 8, FICO 9, FICO 10, FICO 10T, VantageScore 3.0, and VantageScore 4.0 are not all the same.

A lender may use one version, while a monitoring app may show another. This can lead to different scores.

4. The score may have been calculated on a different date

Credit scores can change when new information is reported. If your credit card issuer reports a higher balance this month, your score may change. If a payment posts, an account ages, or an inquiry becomes older, your score may also change.

Even a difference of a few days can matter if your credit reports changed during that time.

5. Not every lender uses the score you see online

Free credit score tools can be useful for tracking general trends, but they may not show the exact score a lender uses. Before applying for major financing, such as a mortgage or auto loan, it is helpful to understand that your application may be evaluated using a different scoring model.

Which Credit Score Do Lenders Use?

Many lenders use FICO Scores, but the exact score model depends on the lender, the credit product, and the lender’s underwriting process. A mortgage lender may use one scoring model, while a credit card issuer or auto finance company may use another.

VantageScore is also used in the marketplace, and its role has grown over time. Some lenders, fintech companies, and financial platforms may use VantageScore for certain decisions, risk evaluations, or account management purposes.

For consumers, the practical lesson is simple: do not assume the score you see in one app is the score every lender will use.

A free credit score can still be valuable. It can help you monitor trends, spot sudden changes, and understand whether your credit profile is generally improving or declining. However, when you are preparing for a major loan, it is wise to review your full credit reports and ask the lender what type of score or credit criteria they use.

What Are FICO 10T and VantageScore 4.0?

FICO 10T and VantageScore 4.0 are newer scoring models that have received more attention because of changes in mortgage credit score modernization.

The “T” in FICO 10T refers to trended data. Trended data looks at patterns in credit behavior over time instead of only looking at a single moment. VantageScore 4.0 also uses trended credit data.

This matters because two consumers may have similar balances on the same day, but very different credit behavior patterns. One person may be steadily paying debt down, while another may be increasing balances month after month. Trended data can help scoring models evaluate those patterns.

For Florida consumers preparing to buy a home, this is important because mortgage lending standards and credit score model usage continue to evolve. Even when these changes do not affect every borrower immediately, they show why long-term credit habits matter.

Instead of focusing only on a quick score boost before applying, consumers should focus on building consistent positive patterns:

- Paying on time every month

- Reducing revolving balances

- Avoiding unnecessary new debt

- Keeping accounts in good standing

- Reviewing credit reports for accuracy

- Addressing credit report errors early

In newer scoring models, your recent and ongoing credit behavior may matter even more because trends can tell a story.

Why Credit Reports Matter More Than Any Single Score

Many consumers focus heavily on the score number. That is understandable. Scores are easy to compare, and lenders often use them as part of a decision.

However, your credit reports are the foundation. Your scores are calculated from the information in your credit reports. If the underlying report data is wrong, your score may not accurately reflect your credit history.

That is why it is important to review all three major credit reports, not just one score.

Common credit report problems may include:

- Accounts that do not belong to you

- Duplicate collection accounts

- Incorrect account balances

- Wrong payment history

- Accounts listed as open when they were closed

- Outdated negative information

- Incorrect personal information

- Mixed credit files

- Debts that were already paid or settled but still report inaccurately

- Collection accounts with missing or questionable details

- Information that cannot be verified

If you find inaccurate, incomplete, outdated, or unverifiable information, you have the right to dispute it with the credit bureaus. Credit repair may help consumers identify and address these types of reporting issues.

FICO Score Factors Explained

Although FICO has different scoring versions, FICO Scores generally evaluate several major credit categories. Understanding these categories can help you make smarter credit decisions.

Payment history

Payment history is one of the most important credit scoring factors. Lenders want to know whether you have paid past accounts on time.

Late payments, charge-offs, collections, repossessions, foreclosures, and other serious negative items may hurt your score. The impact can depend on the severity, frequency, recency, and overall credit profile.

A single late payment may affect one person differently than another, depending on the rest of the credit file. However, consistently paying on time is one of the strongest habits for long-term credit health.

Amounts owed

Amounts owed often refers to how much debt you carry, especially compared to your available credit limits. Credit card utilization is a major part of this category.

For example, if you have a credit card with a $1,000 limit and a $900 balance, your utilization on that card is 90%. High utilization can make you appear more financially stretched.

Lower utilization is generally better for credit scores. Many consumers focus on keeping balances below 30% of available credit, but lower may be better depending on the scoring model and credit profile.

Length of credit history

Scoring models may consider how long your accounts have been open. Older accounts can help show a longer track record of credit management.

This is why closing old positive accounts can sometimes affect your credit profile. It may reduce available credit and eventually affect the age of accounts considered in scoring.

Credit mix

Credit mix refers to the variety of accounts on your credit reports. For example, a credit profile may include credit cards, auto loans, student loans, mortgages, or personal loans.

You do not need every type of account to have good credit. However, responsibly managing different types of credit can support a stronger profile.

New credit

Applying for new credit can create hard inquiries. Too many hard inquiries in a short period may affect your score and may signal increased risk to lenders.

Opening several new accounts quickly can also lower your average account age. This does not mean you should avoid new credit forever, but it does mean you should apply strategically.

VantageScore Factors Explained

This scoring model also considers credit report information, but it organizes and weights the factors differently.

Common VantageScore factors include:

- Payment history

- Depth of credit

- Credit utilization

- Balances

- Recent credit

- Available credit

Payment history is highly important. Credit utilization and balances can also have a significant impact. Like FICO, VantageScore generally rewards responsible credit use and penalizes signs of higher risk, such as missed payments or excessive revolving debt.

One important feature of VantageScore 4.0 is its use of trended credit data. This can help evaluate patterns in how consumers manage balances and payments over time.

For example, if your balance is high today but you have been consistently paying it down, that trend may tell a different story than a high balance that keeps increasing.

Why Free Credit Scores May Not Match Lender Scores

Many people become frustrated when a free app shows one score and a lender gives them another. This is one of the most common credit score misunderstandings.

Free scores are not useless. They can be very helpful for monitoring general credit direction. If your score drops suddenly, it may alert you to a new balance, missed payment, inquiry, collection, or possible reporting error.

However, free scores may differ from lender scores because:

- The app may show VantageScore while the lender uses FICO.

- The app may use TransUnion data while the lender uses Experian or Equifax.

- The score may be updated weekly while the lender pulls a fresh score today.

- The lender may use an industry-specific score.

- The lender may use a different scoring version.

- The lender may consider other factors beyond the score.

This is why consumers should treat free scores as educational tools, not as guaranteed lender approval numbers.

FICO vs. VantageScore for Mortgages

Mortgage lending has historically relied heavily on FICO scoring models. However, the mortgage industry has been moving toward updated scoring models, including FICO 10T and VantageScore 4.0.

This shift is important because newer models may evaluate credit data differently than older models. In particular, trended data may play a greater role.

For homebuyers, the lesson is not to panic or chase a specific score model. Instead, focus on the credit behaviors that generally help across scoring models:

- Pay every account on time.

- Lower credit card balances.

- Avoid opening unnecessary accounts before applying.

- Do not make large credit changes without speaking to your mortgage professional.

- Review all three credit reports well before applying.

- Address possible reporting errors early.

If you are planning to buy a home in Florida, it is smart to begin reviewing your credit months in advance. Waiting until a few weeks before applying may not leave enough time to correct errors or improve financial habits.

FICO vs. VantageScore for Auto Loans

Auto lenders may use FICO Scores, VantageScore, or industry-specific scoring models. Some auto lenders use FICO Auto Scores, which are designed specifically for vehicle financing decisions.

This means the score you see online may not be the same score used at a dealership or credit union.

If you are preparing to finance a car, pay attention to your credit reports, not just the score. Auto lenders may review your payment history, current debts, income, down payment, loan amount, and prior auto loan history.

Before applying, it may help to:

- Review your credit reports

- Pay down revolving balances if possible

- Avoid unnecessary new credit

- Compare financing options

- Understand the difference between prequalification and final approval

- Ask lenders whether they use a soft pull or hard pull

FICO vs. VantageScore for Credit Cards

Credit card issuers may use different scoring models depending on their underwriting systems. Some may use FICO, some may use VantageScore, and some may use internal models combined with credit bureau data.

Credit card approval decisions often consider more than the score. Issuers may also look at income, existing debt, recent applications, prior relationship with the bank, and current credit limits.

Credit card balances can have a strong effect on both FICO and VantageScore. Because credit cards are revolving accounts, utilization can change month to month. Paying down high balances may help your credit profile, but the timing of when your card issuer reports the balance can matter.

For example, paying your balance after the statement closes may still result in a higher balance being reported. If you are preparing for a credit application, it may be useful to understand your statement closing dates and payment due dates.

Which Score Should Florida Consumers Pay Attention To?

Florida consumers should pay attention to both FICO Score and VantageScore, but they should not obsess over one number.

The better approach is to monitor:

- Your credit reports from Equifax, Experian, and TransUnion

- Your payment history

- Your credit card utilization

- Your account balances

- New inquiries

- Collections or charge-offs

- Identity theft warning signs

- Incorrect or unfamiliar accounts

Your score is the result of the information in your reports. If your reports improve, your scores may improve over time depending on the scoring model. If your reports contain negative or inaccurate information, your scores may be affected.

This is especially important for consumers who are rebuilding after financial hardship, debt settlement, bankruptcy, divorce, medical debt, identity theft, job loss, or collection activity.

How Credit Report Errors Can Affect FICO and VantageScore

Credit report errors can affect more than one scoring model. Since both FICO and VantageScore rely on credit report data, inaccurate information may influence multiple scores.

For example, if a collection account appears on your report but does not belong to you, that account could affect both FICO and VantageScore calculations. If a credit card reports the wrong balance or limit, your utilization may appear higher than it really is.

Common errors that may affect scores include:

- Incorrect late payments

- Duplicate debts

- Accounts from identity theft

- Wrong account status

- Incorrect charge-off dates

- Paid accounts still showing unpaid

- Settled accounts reporting inaccurately

- Old debts reappearing with incorrect dates

- Mixed files with another person’s information

- Incorrect collection agency reporting

These issues can be frustrating, especially if you are preparing for financing. Credit repair focuses on reviewing credit reports and challenging information that may be inaccurate, incomplete, outdated, or unverifiable.

How to Improve Both FICO Score and VantageScore

While FICO and VantageScore are different, many responsible credit habits can help support both.

Pay every bill on time

On-time payment history is one of the strongest credit habits. Even one missed payment can hurt, especially if it becomes 30 days late or more.

Set reminders, use autopay when appropriate, and contact creditors early if you are experiencing hardship.

Keep credit card balances low

Credit utilization can strongly affect credit scores. If possible, keep balances low compared to limits.

This does not mean you need to carry a balance. In fact, carrying a balance can cost interest. Paying in full may help you avoid interest charges while supporting responsible credit use.

Avoid applying for too much new credit at once

Multiple applications in a short time can create hard inquiries and may lower the average age of your accounts. Apply for credit strategically.

If you are shopping for a mortgage or auto loan, ask lenders how rate shopping inquiries may be handled.

Keep older positive accounts open when possible

Older accounts can help your credit profile. If an older account has no annual fee and is in good standing, keeping it open may help preserve available credit and account age.

However, this depends on your personal financial situation. If a card has high fees or creates overspending risk, closing it may still make sense.

Review all three credit reports

Do not rely only on one score or one bureau. Review Equifax, Experian, and TransUnion.

Look for unfamiliar accounts, inaccurate balances, outdated negative items, and duplicate collections.

Dispute inaccurate information

If you find information that is inaccurate, incomplete, outdated, or unverifiable, you may dispute it with the credit bureaus.

When disputing, include clear explanations and supporting documentation when available.

Avoid illegal credit repair tactics

Be cautious of anyone promising a “new credit identity,” guaranteed score increases, instant deletions, or methods involving false identity information. These tactics can be illegal and harmful.

Legitimate credit repair focuses on your rights, accurate reporting, and the dispute process.

What Credit Repair Can and Cannot Do

Credit repair can help consumers review their credit reports and challenge information that may be inaccurate, incomplete, outdated, or unverifiable.

Credit repair may help when your credit reports contain:

- Incorrect late payments

- Accounts that are not yours

- Duplicate collections

- Outdated negative accounts

- Unverifiable account information

- Mixed-file information

- Incorrect balances or statuses

- Identity theft-related accounts

However, credit repair cannot legally guarantee a specific score increase. Credit repair cannot erase accurate and timely negative information simply because it is hurting your score. Creating a new legal credit identity is not something legitimate credit repair can do. Lender approval also cannot be forced or guaranteed.

A compliant credit repair process should be based on accuracy, documentation, consumer rights, and proper communication with credit bureaus, furnishers, and collection agencies.

At Credit Repair of Florida, the goal is to help consumers better understand their credit reports, identify questionable information, and take informed steps toward a more accurate credit profile.

Why Your Credit Score May Drop Even When You Are Doing the Right Things

Sometimes a credit score changes in ways that feel unfair. You may pay a bill, close an account, or reduce debt and still see a temporary drop.

Here are some common reasons:

- A credit card balance increased before the statement closed.

- An old account was closed and reduced your available credit.

- A new hard inquiry appeared.

- A new account lowered your average account age.

- A collection was added.

- A credit limit decreased.

- A lender updated old account information.

- Different scoring models reacted differently to the same change.

This is why it is important to look beyond the number and review what changed on your credit reports.

Why Scores Can Differ Between Equifax, Experian, and TransUnion

Even if the same scoring model is used, scores can differ across the three credit bureaus because the underlying credit reports may differ.

One bureau may show:

- A different balance

- A different credit limit

- A missing account

- An extra collection

- A different inquiry

- A different payment update date

- An account that has not been updated yet

Because lenders are not always required to report to all three bureaus, differences are common. This is also why reviewing all three reports matters.

Should You Worry If Your VantageScore Is Higher Than Your FICO Score?

Not necessarily. It is common for one score to be higher than another.

A higher VantageScore does not automatically mean a lender will approve you. A lower FICO Score does not automatically mean your credit is terrible. Scores must be understood in context.

Instead of focusing only on the difference, ask:

- Which credit bureau is each score based on?

- Which scoring version is being used?

- When was each score updated?

- Did any account recently change?

- Are there errors on one report but not another?

- Which score does the lender actually use?

The most important step is to keep your reports accurate and your financial habits consistent.

Should You Worry If Your FICO Score Is Higher Than Your VantageScore?

Again, not necessarily. The models are different. One may respond more strongly to certain information than the other.

If your FICO Score is higher than your VantageScore, review your credit reports for the same issues:

- High balances

- Recent late payments

- New inquiries

- Collections

- Account age

- Credit limits

- Incorrect reporting

The difference itself is not always a problem. The reason behind the difference is what matters.

How to Prepare Your Credit Before Applying for a Mortgage in Florida

If you plan to buy a home in Florida, begin preparing your credit early. Mortgage underwriting can be detailed, and credit score requirements may vary by loan type, lender, and borrower profile.

Here are steps to consider:

- Review all three credit reports several months before applying.

- Look for inaccurate, incomplete, outdated, or unverifiable information.

- Avoid opening unnecessary new credit accounts.

- Avoid large credit card balances.

- Pay all accounts on time.

- Do not co-sign new debt before applying.

- Keep financial documents organized.

- Speak with a licensed mortgage professional about loan requirements.

- Avoid making major financial changes without guidance.

Credit preparation is not just about the score. Lenders may review your debt-to-income ratio, employment, income, assets, down payment, reserves, and credit history.

How to Prepare Your Credit Before Applying for an Auto Loan

Before applying for an auto loan, review your credit reports and understand your budget.

Dealership financing can involve multiple lender submissions, so ask questions before authorizing credit pulls. Compare offers from banks, credit unions, and online lenders when possible.

To prepare:

- Check your reports for errors.

- Pay down credit card balances if possible.

- Avoid new unnecessary accounts.

- Save for a down payment.

- Know your realistic monthly payment.

- Review total loan cost, not just the payment.

- Be cautious with extended loan terms that may increase total interest.

A better credit profile may help you qualify for more favorable terms, but every lender has its own criteria.

How to Prepare Your Credit Before Applying for a Credit Card

Before applying for a credit card, check whether the issuer offers prequalification. Prequalification may use a soft inquiry, although final approval usually requires a hard inquiry.

Consider:

- Your current credit score range

- Recent inquiries

- Current balances

- Existing credit limits

- Annual fees

- Interest rates

- Rewards programs

- Whether the card fits your spending habits

- Avoid applying for multiple cards just to see what happens. Too many applications may hurt your credit profile.

Common Myths About FICO and VantageScore

Myth 1: You only have one credit score

You have many possible credit scores. Scores vary by model, version, bureau, and date.

Myth 2: The score in my app is the score every lender sees

Not always. Many apps show educational scores or VantageScore models. Lenders may use different models.

Myth 3: Checking your own score hurts your credit

Checking your own credit is generally considered a soft inquiry and does not hurt your score.

Myth 4: Closing a credit card always helps

Closing a credit card can reduce available credit and may increase utilization. It may help in some situations, but it is not automatically good for your score.

Myth 5: Carrying a balance improves your credit

You do not need to carry a balance and pay interest to build credit. Responsible use and on-time payments matter.

Myth 6: Credit repair can guarantee a score increase

No legitimate credit repair company should guarantee a specific score increase. Results depend on your credit reports, the accuracy of the information, and how bureaus and furnishers respond.

FICO vs. VantageScore: Which One Is More Important?

There is no single answer for every consumer.

FICO may be more important if your lender uses FICO. VantageScore may be more relevant if a lender, platform, or monitoring tool uses VantageScore. For mortgage lending, changes involving FICO 10T and VantageScore 4.0 make it important to understand both.

Instead of choosing one score to care about, focus on what both models have in common:

- They rely on credit report data.

- They reward on-time payments.

- They are affected by high revolving balances.

- They may react to recent credit applications.

- They may be hurt by serious negative information.

- They depend on accurate reporting.

If you build a stronger, cleaner, more accurate credit profile, you are generally supporting both types of scores.

When to Get Help With Credit Report Issues

You may want help if:

- You do not understand what is on your credit reports.

- You see accounts you do not recognize.

- You have duplicate collections.

- You have old debts still reporting.

- You believe an account is reporting inaccurately.

- You were denied credit because of report information.

- You are preparing for a mortgage or auto loan.

- You experienced identity theft.

- You are overwhelmed by the dispute process.

Credit repair is not magic, and it is not instant. However, professional support can help consumers understand their reports, organize disputes, and address questionable information more effectively.

Final Thoughts: Understanding the Difference Can Help You Make Better Credit Decisions

FICO Score and VantageScore are both important credit scoring models, but they are not the same. They may use similar score ranges, but they can calculate scores differently, rely on different versions, and be used by different lenders.

The score you see online can be helpful, but it may not be the exact score used for a mortgage, auto loan, credit card, or rental decision. That is why consumers should pay close attention to their full credit reports, not just one score.

For Florida consumers, the best strategy is to build strong credit habits over time, monitor all three credit reports, correct inaccurate information, and avoid risky shortcuts.

At Credit Repair of Florida, we help consumers review their credit reports and identify inaccurate, incomplete, outdated, or unverifiable information that may be affecting their credit. If you are unsure why your scores are different or you believe your credit reports contain errors, our team can help you understand your options and take the next step.

Frequently Asked Questions About FICO Score vs. VantageScore

Is FICO better than VantageScore?

Not necessarily. FICO and VantageScore are different credit scoring models. FICO Scores are widely used by lenders, while VantageScore is also used in the marketplace and commonly shown by free credit monitoring platforms. The most important score is the one your specific lender uses.

Why is my VantageScore different from my FICO Score?

Your scores may differ because FICO and VantageScore use different formulas. They may also be based on different credit bureau data, different scoring versions, or different update dates.

Why is my VantageScore higher than my FICO Score?

A VantageScore may be higher because the model weighs your credit information differently. It may also be based on a different credit bureau report or a more recent update. A higher VantageScore does not guarantee that a lender using FICO will see the same number.

Why is my FICO Score higher than my VantageScore?

Your FICO Score may be higher because of differences in scoring formulas, bureau data, account updates, or the specific scoring version being used. The difference is not always a sign of an error, but it is worth reviewing your credit reports for accuracy.

Do mortgage lenders use FICO or VantageScore?

Mortgage lenders have historically relied heavily on FICO scoring models, but newer models such as FICO 10T and VantageScore 4.0 are increasingly relevant due to mortgage credit score modernization. The exact score used can depend on the lender, loan program, and current guidelines.

Do auto lenders use FICO or VantageScore?

Auto lenders may use FICO, VantageScore, industry-specific scores, or internal lending models. Some auto lenders use FICO Auto Scores. Before applying, it can help to ask the lender what type of credit score they use.

Do credit card companies use FICO or VantageScore?

Credit card companies may use different scoring models depending on their underwriting systems. Some may use FICO, some may use VantageScore, and some may combine credit scores with internal risk models.

Does checking my own credit score hurt my credit?

Checking your own credit score is generally considered a soft inquiry and does not hurt your credit score. Hard inquiries usually occur when you apply for credit and a lender reviews your credit report for a lending decision.

Can credit repair improve both FICO and VantageScore?

Credit repair may help if inaccurate, incomplete, outdated, or unverifiable information is corrected or removed from your credit reports. Since both FICO and VantageScore rely on credit report data, more accurate reporting may affect scores. However, no company can guarantee a specific score increase.

Which score should I monitor?

It is helpful to monitor both your scores and your credit reports. Your reports are especially important because they contain the information used to calculate your scores. Review Equifax, Experian, and TransUnion regularly to check for errors or unfamiliar activity.

What is the fastest way to improve my credit score?

There is no guaranteed quick fix, but some actions may help over time. Paying bills on time, reducing high credit card balances, avoiding unnecessary new credit, and disputing inaccurate credit report information can support a healthier credit profile.

Why did my credit score drop after paying off debt?

Your score may change after paying off debt because scoring models consider many factors, including account mix, utilization, account status, and reporting updates. Paying debt is usually positive for your finances, but the score impact can vary depending on your credit profile.

Is VantageScore 4.0 important?

Yes, VantageScore 4.0 is important because it uses trended credit data and is part of broader credit score modernization discussions. Consumers should understand that newer models may look more closely at credit behavior patterns over time.

Is FICO 10T important?

Yes, FICO 10T is important because it also uses trended credit data. This means long-term balance and payment patterns may matter, especially as newer scoring models become more widely used.

What should I do if my credit reports have errors?

If your credit reports contain inaccurate, incomplete, outdated, or unverifiable information, you can dispute the information with the credit bureaus. You may also work with a credit repair professional to help review your reports and organize the dispute process.

References

FICO. “About FICO Scores.”

myFICO. “What’s in Your FICO Score?”

VantageScore. “VantageScore 4.0.”

VantageScore. “Releasing the Power of Trended Credit Data.”

Consumer Financial Protection Bureau. “What Is the Difference Between a Credit Report and a Credit Score?”

Federal Housing Finance Agency. “Credit Scores.”

Federal Trade Commission. “Fixing Your Credit FAQs.”

Federal Trade Commission. “Disputing Errors on Your Credit Reports.”

AnnualCreditReport.com. “Official Free Credit Reports.”